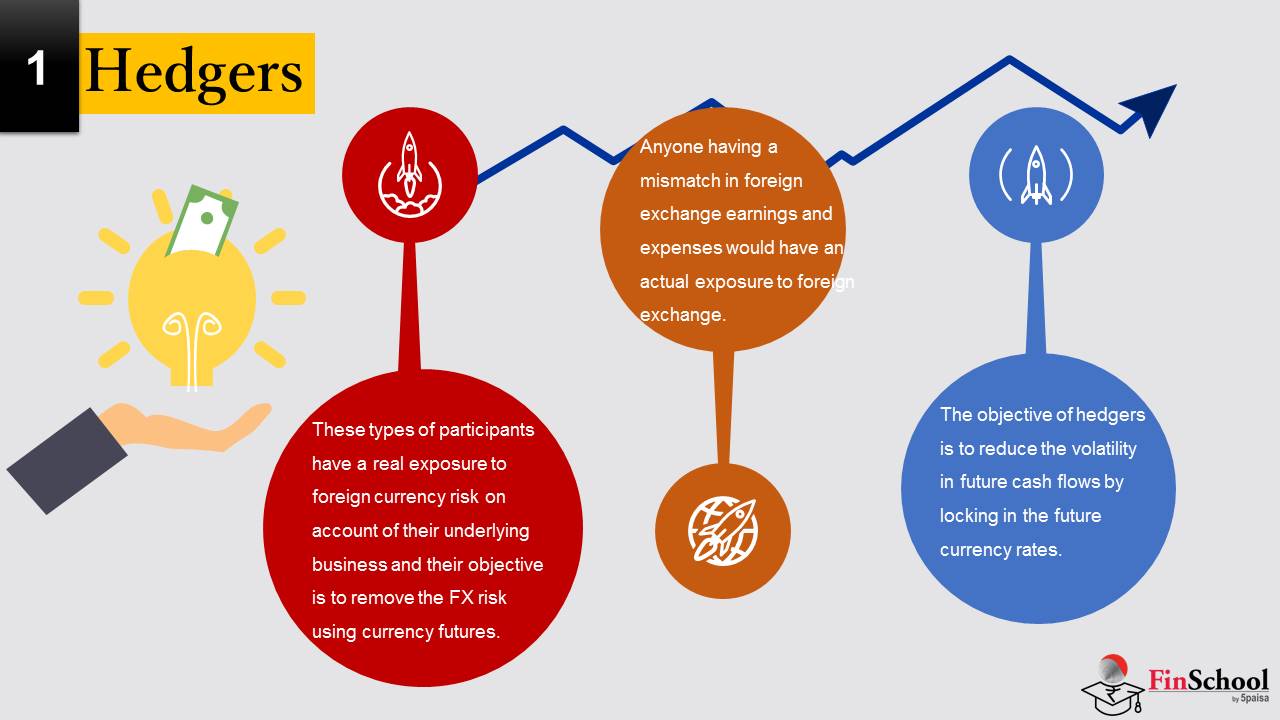

5.1 Hedgers

These types of participants have a real exposure to foreign currency risk on account of their underlying business and their objective is to remove the FX risk using currency futures. The exposure could be because of imports/ exports of goods/services, foreign investments or foreign expenditure on account of travel, studies or any other type of need resulting in FX exposure. In other words, anyone having a mismatch in foreign exchange earnings and expenses would have an actual exposure to foreign exchange. The objective of hedgers is to reduce the volatility in future cash flows by locking in the future currency rates. For example, a shoe exporter from India buys all its raw material domestically and sells all its goods to Europe. For him, the expenditure is in INR while revenue is in EUR. Assume he has shipped an order of EUR 1 million for which payment will be received after 3 months. During the 3 month credit period, shoe exporter is carrying the risk of EURINR price movement. He is interested to hedge the currency price risk. In this example, the shoe exporter is a hedger.

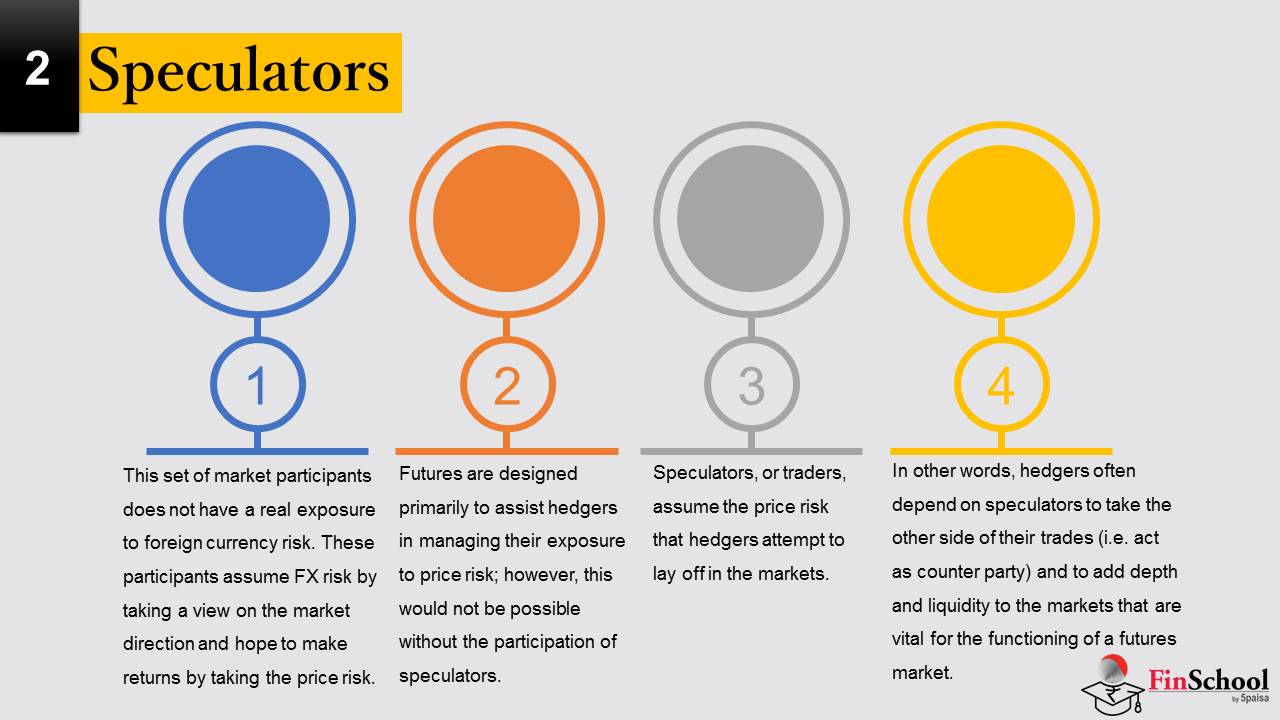

5.2 Speculators

This set of market participants does not have a real exposure to foreign currency risk. These participants assume FX risk by taking a view on the market direction and hope to make returns by taking the price risk. Speculators play a vital role in the futures markets. Futures are designed primarily to assist hedgers in managing their exposure to price risk; however, this would not be possible without the participation of speculators. Speculators, or traders, assume the price risk that hedgers attempt to lay off in the markets. In other words, hedgers often depend on speculators to take the other side of their trades (i.e. act as counter party) and to add depth and liquidity to the markets that are vital for the functioning of a futures market.

5.3 Arbitrageurs

This set of market participants identify mispricing in the market and use it for making profit. They have neither exposure to risk and nor do they take the risk. Arbitrageurs lock in a profit by simultaneously entering opposite side transactions in two or more markets. For example, if the relation between forward prices and futures prices differs, it gives rise to arbitrage opportunities. Difference in the equilibrium prices determined by the demand and supply at two different markets also gives opportunities to arbitrage. As more and more market players will realize this opportunity, they may also implement the arbitrage strategy and in the process will enable market to come to a level of equilibrium and the arbitrage opportunity may cease to exist.

Each of these participants has different risk profile.

- The hedger is the most conservative participant in the currency futures market as they have an underlying currency exposure and hence run currency risk. Their motivation to participate in currency futures is to purely manage the risk and not to make any profit out of the transaction.

- The trader is the high risk participant and takes positions in the currency futures based on their view of currencies.

- The arbitrageurs have lower risk profile because they buy in the spot market and sell in the futures or they can even arbitrage between forwards and futures. Arbitrage is like fixed-income because the arbitrageur only tries to play on the spread between two prices of a currency pair.

5.4 Positions That Can Be Taken In Futures Market

Hedging in currency market can be done through two positions i.e short hedge & long hedge

Short Hedge

Taking a short position in the futures market is referred to as a short hedge. In a currency market, a short hedge is taken by someone who already possesses or expects to receive the base currency in the future.

It is typically appropriate for a hedger to use when an asset is expected to be sold in the future. Alternatively, it can be used by a speculator who anticipates that the price of a contract will decrease.

For example, assume a cattle rancher plans to sell a pen of feeder cattle in March based on the spot prices at that time. The rancher can hedge in the following manner. Currently

- A March futures contract is purchases for a price of $150

- For simplicity, assume the rancher antipates (and does sell) selling 50,000 pounds (1 contract)

- Spot prices are currently $155

- What happens when the spot price is March decreases to $140?

– Rancher loses $10 per 100 pounds on the sale from the decreased price

– Rancher gains $10 by selling the futures contract for $150 and immediately buying (to close out) for $140

– Effective price of the sale is $150

- What happens when the spot price is March increases to $160?

– Rancher gains $10 per 100 pounds on the sale from the increased price

– Rancher loses $10 by buying the futures contract for $150 and immediately selling (to close out) for $160

– Effective price of the sale is $150

- The seller has effectively locked in on the price prior to the sale by offsetting gains/losses

Now assume the same for a speculator who takes a short position on a March futures contract at $150

- If the price falls to $140, the speculator sells for $150 and immediately buys for $140, leading to a gain of $10 per 100 pounds [$5,000 gain in value for one contract]

- If the price increases to $160, the speculator loses $5,000

Long Hedge

Holding a long position in the futures market is referred to as a long hedge. A Long position holder promises to pay the specified exchange rate to purchase the currency pair at the expiration date. Those who will need to buy base currency in the future to pay any liabilities will employ this technique.

A long hedge is a cost-cutting approach for a corporation that knows it will need to buy a commodity in the future and wants to lock in the price. The hedge is straightforward: the buyer of a commodity simply takes a long futures position. A long position suggests the commodities buyer is betting on the price of the commodity rising in the future. If the price of good rises, the profit from the futures trade helps to cover the higher cost.

It is typically appropriate for a hedger to use when an asset is expected to be bought in the future. Alternatively, it can be used by a speculator who anticipates that the price of a contract will increase.

For example, assume an oil producer plans on purchasing 2,000 barrels of crude oil in August for a price equal to the spot price at the time.

The producer can hedge in the following manner by using crude oil futures from the NYMEX. Currently,

- An August oil futures contract is purchases for a price of $59 per barrel • Spot prices are currently $60

- What happens when the spot price in August decreases to $55?

– Producer gains $4 per barrel on the purchase from the decreased price

– Producer loses $4 by buying the futures contract for $59 and immediately selling (to close out) for $55

– Effective price of the sale is $59

- What happens when the spot price in August increases to $65?

– Producer loses $6 per barrel on the purchase from the increased price

– Producer gains $6 by selling the futures contract for $59 and immediately buying (to close out) for $65

– Effective price of the sale is $59

- The producer has effectively locked in on the price prior to the sale by offsetting gains/losses

Now assume the same for a speculator who takes a long position on a March futures contract at $59

- If the price increases to $65, the speculator sells for $59 and immediately buys for $65, leading to a gain of $6 per barrel [$12,000 gain in value for five contracts]

- If the price increases to $55, the speculator loses $12,000

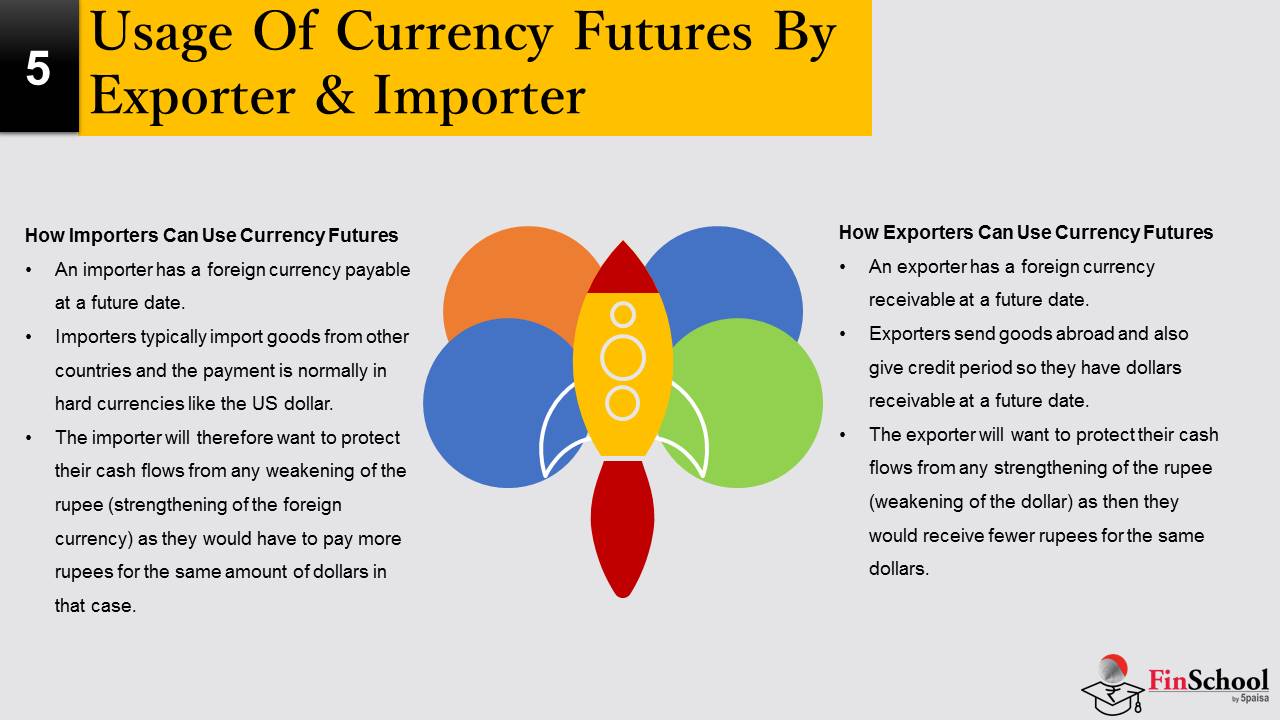

5.5 Usage Of Currency Futures By Exporter & Importer

Foreign currency risk arises either if you have a foreign currency payable at a future date or a foreign currency receivable at a future date. An importer has a foreign currency payable at a future date while an exporter has a foreign currency receivable at a future date. Like the importer, a foreign currency borrower also has a foreign currency payable at a future date.

How importers can use currency futures

An importer has a foreign currency payable at a future date. Importers typically import goods from other countries and the payment is normally in hard currencies like the US dollar. The importer will therefore want to protect their cash flows from any weakening of the rupee (strengthening of the foreign currency) as they would have to pay more rupees for the same amount of dollars in that case. Let us look at the case study below.

Illustration 1: XYZ imports machine parts from the US and has to pay them in fixed dollars after a credit period of 3 months. In August 2019, XYZ imported parts worth $1,000,000 when the exchange rate was Rs.72/$. How can XYZ use currency futures to protect the underlying risk?

Strategy 1: Since the importer has dollar payables at the end of 3 months, they would be wary of rupee weakening. If rupee weakens from Rs.72 to Rs.77 in the next 3 months, then XYZ will require Rs.7.70 crore after 3 months to obtain the same $1 million and the company is not prepared for that. The answer would be to buy USDINR futures with 3 months expiry. This is how it would work.

Let us assume that the USDINR futures (3 months) are currently trading at Rs.72.50. Since the lot size of USDINR futures is $1000, they will need to buy 1000 lots to hedge the risk of $1 million payable at the end of 3 months.

Strategy Payoff 1: To understand the payoff to XYZ at the end of 3 months, let us assume that the rupee weakens to $80/$ due to a sharp rise in trade deficit. Now what happens at the end of 3 months?

Bought 1000 lots of USDINR futures at Rs.72.50 worth Rs.7.25 crore notional values.

At the end of 3 months, the spot dollar is at Rs.80/$. So, XYZ will need Rs.8 crore to purchase $1 million worth of dollars to pay the client.

But since XYZ is long on USDINR 3 month futures, at Rs.72.50, this can be offloaded in the currency futures market at (say Rs.80.20). The gain on currency futures will be:

(80.20 – 72.50) X 1000 lots X $1000 per lot = Rs.77 lakhs (profit on long USDINR futures)

How the hedge works 1:

Total rupee outflow at the end of 3 months for $1 million = Rs.8 crore (@Rs.80/$)

Less: profit on long USDINR futures = Rs.77 lakhs

Net outflow for the importer = Rs.7.23 crore

In the above case, by hedging with long USDINR futures, XYZ has locked in its cost at around the rate 3 months back. That is how hedging works for the importer. What if the rupee had appreciated; would the importer not have lost? That is correct, but the purpose of hedging is not to make profits but to have predictable cash flows.

How exporters can use currency futures

An exporter has a foreign currency receivable at a future date. Exporters send goods abroad and also give credit period so they have dollars receivable at a future date. The exporter will want to protect their cash flows from any strengthening of the rupee (weakening of the dollar) as then they would receive fewer rupees for the same dollars.

Illustration 2: ABC Ltd. exports garments to the US and receives in fixed dollars after a credit period of 3 months. In August 2019, ABC exported garments worth $1,000,000 when the exchange rate was Rs.72/$. How to use currency futures in this case?

Strategy 2: Since the exporter has dollar receivables at the end of 3 months, they would be wary of rupee strengthening. If rupee strengthens from Rs.72 to Rs.67 in the next 3 months, then ABC will able to convert $1 million into just Rs.6.70 crore. The answer would be to sell USDINR futures with 3 months expiry.

Let us assume that the USDINR futures (3 months) are currently trading at Rs.72.50. Since the lot size of USDINR futures is $1000, they will need to sell 1000 lots to hedge the risk of $1 million receivable at the end of 3 months.

Strategy Payoff 2: To understand the payoff to ABC at the end of 3 months, let us assume that the rupee strengthens to Rs.66/$ due to heavy FPI and FDI inflows. What happens at the end of 3 months?

ABC sold 1000 lots of USDINR futures at Rs.72.50 worth Rs.7.25 crores of notional value.

At the end of 3 months, the spot dollar is at Rs.66/$. So, ABC will get just Rs.6.60 crore against $1 million and that will be insufficient for onward payments.

But since ABC is short on USDINR 3 month futures, at Rs.72.50, this can be offloaded in the currency futures market at (say Rs.66.20). The gain on currency futures will be:

(72.50 – 66.20) X 1000 lots X $1000 per lot = Rs.63 lakhs (profit on USDINR futures)

How the hedge works 2:

Total rupee inflow at the end of 3 months for $1 million = Rs.6.60 crore (@Rs.66/$)

Add: profit on short USDINR futures = Rs.63 lakhs

Net inflow for the exporter = Rs.7.23 crore

The exporter, by hedging by selling USDINR futures, has locked in cost at around the rate 3 months back. That is how hedging works for the exporter. What if the rupee had weakened; would the exporter not have lost? That is correct, but again this is about predictable cash flows.

Use of currency futures by arbitrageurs

As mentioned earlier, arbitrageurs look for mispricing in the market and execute simultaneous buy and sell to capture the mispricing and make profit. They do not take any view on the market direction. Let us take an example.

A trader notices that 6 month USDINR currency futures was trading at 45.98/46 while 6 month forward in OTC market, for same maturity as that of currency futures contract, was available at 45.85/86. Let us answer few questions on this scenario.

Is there an opportunity to make money in the scenario given above? If yes, what trade can be executed to make money? Ideally currency futures and currency forward should be trading at same level, it their settlement dates are same. A difference in pricing means mispricing and an opportunity to set an arbitrage trade to capture the mispricing and make money by selling the market where the price is higher and buying in the market where the price is lower.

The trader could short currency futures and go long on currency forward to capture the mispricing. How much profit per USD could be trader make by setting an arbitrage trade if the settlement price of currency futures was 47 and the OTC contact was also settled at 47? The trader would short currency futures at price of 45.98 and go long in currency forward at 45.86. At the time of settlement, trader loses 1.02 on futures and makes a profit of 1.14 on OTC forward contract. Thus he makes an arbitrage profit of 0.12 per USD.

Please note that arbitrage profit would have been constant at 0.12 irrespective of final settlement price as long as both OTC contract and futures contract were settled at the same price.

Since execution of arbitrage trade requires simultaneous buy and sell of a contract, there is a loss of value in paying bid-ask difference. As you would have noticed in the above example, the trader pays two paise bid-ask in futures contract and pays one paise in OTC contract. Therefore arbitrageurs prefer to execute the trade through the brokers/ exchanges/ trading terminals etc which offers prices at the least possible bidask difference.